Before the conflict kicked off in the Middle East, February delivered strong gains for Australian equities and select global markets. Investors moved away from technology stocks and towards mining, energy and other physical industries, with Australia among the beneficiaries. The US lagged, weighed down by technology weakness and tariff uncertainty. Late in the month, military escalation in the Middle East drove a sharp spike in volatility, leaving markets unsettled heading into March.

Be sure to come back for our March update to find out how the Middle East conflict has continued to impact markets throughout the month.

Economic Conditions

The Reserve Bank of Australia raised its cash rate by 0.25% in February (and then again by 0.25% to 4.10% in March), its first increase since 2023 and the only major central bank to do so. Inflation is still not within its target band.

In the US, the Federal Reserve left rates unchanged. Trade policy and tariffs were a dominant story through the month, with the US Supreme Court striking down President Trump’s tariffs only for new ones to be imposed within hours under different authority.

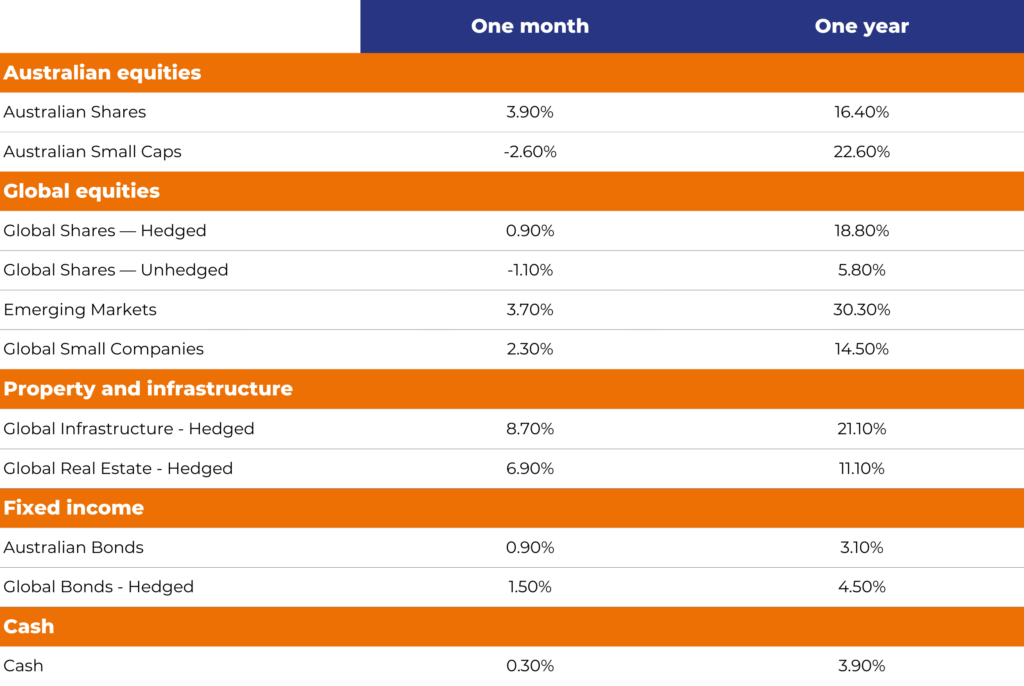

The Australian dollar rose 1.7% against the US dollar in February, pushing through US$0.71 for the first time in three years. A rising Australian dollar reduces the returns that Australian investors receive from overseas assets held without currency hedging. This is why global shares returned 0.9% for hedged investors but fell 1.1% for those without currency protection, despite underlying markets rising.

Tensions in the Middle East escalated in the final days of February and triggered retaliatory strikes across the region, effectively closing the Strait of Hormuz. The Strait carries around a fifth of the world’s oil supply, and a significant share of global fertiliser trade also passes through it. Oil prices rose sharply, adding further pressure on inflation. The situation remains active and is the key source of uncertainty for investors in the months ahead.

Equities

Australia was among the clear beneficiaries of the month’s shift in investor sentiment. The ASX rose 3.9%, led by materials and mining companies, and by banks which were boosted by the RBA rate rise. Markets in Japan, Europe and the emerging world also performed well.

The United States was the exception. Technology stocks sold off in response to the launch of new AI tools capable of performing tasks that businesses currently pay expensive software subscriptions to handle. This triggered questions about the long-term viability of those business models, sending software valuations sharply lower.

Fixed Interest

Bonds had a strong month. As uncertainty rose through February, investors moved into the relative safety of government bonds, pushing prices higher. Australian bonds returned 0.9% and global bonds 1.5%. The interest being paid on bonds and other defensive investments remains close to levels not seen for over a decade. Beyond the income they generate, when share markets come under pressure, bonds have historically moved in the opposite direction, helping to cushion the impact on a diversified portfolio.

Since month end, the Middle East escalation has pushed energy prices and inflation expectations higher, causing yields to rise and unwinding some of those gains. The income investors receive from bonds, however, remains intact.

Winners & Losers

Infrastructure and global listed property were the standout performers, rising 8.7% and 6.9% respectively. Both benefited from the broad rotation away from technology stocks, as investors favoured assets with physical backing and reliable income streams. Government spending on physical infrastructure continues to grow globally, and demand for data centres and power networks driven by AI investment provided an additional tailwind. Gold rose 3.0% for the month and is up 60.5% over the past year, supported by a weaker US dollar and growing geopolitical uncertainty.

US shares and global technology stocks fell, as covered in the Equities section. Australian listed property also declined through the month, as higher interest rates weighed on borrowing costs and property valuations. Australian small caps declined 2.6% for the month, though they have gained 22.6% over the past year.

Asset Class Returns – February 2026