MARCH 2026

The story of March was the escalation of the conflict in the Middle East and the closure of the Strait of Hormuz. Shares fell broadly, bonds came under pressure as inflation expectations rose, and the US dollar strengthened.

Share market pullbacks are a normal and expected feature of investing in equities. Geopolitical events have periodically tested markets throughout history, and the evidence is consistent: the initial reaction tends to be larger than the lasting economic damage. Volatility of this kind is unsettling, but markets have recovered from every major conflict-driven selloff on record. Maintaining a long-term perspective and staying invested through periods of short-term noise has historically been the most reliable course.

Economic conditions

The Reserve Bank of Australia raised its cash rate by 0.25% to 4.1% in March, its second consecutive increase, as persistent domestic inflation was compounded by the surge in energy prices. Based on current market pricing, further increases remain a strong possibility.

In the US, the economy was already slowing before the Iran shock, with growth weakening and inflation remaining sticky. With current inflation data largely compiled before oil prices surged, the full effect of the energy shock is not yet visible in the official figures.

The full impact of the conflict remains uncertain and, with the situation continuing to evolve, will depend on how events unfold. Beyond energy, the disruption affects fertiliser and other commodities critical to global food production, meaning the inflationary implications extend well beyond the oil price alone. Higher input costs will take time to feed through to businesses and households alike, and those effects are still emerging.

Equities

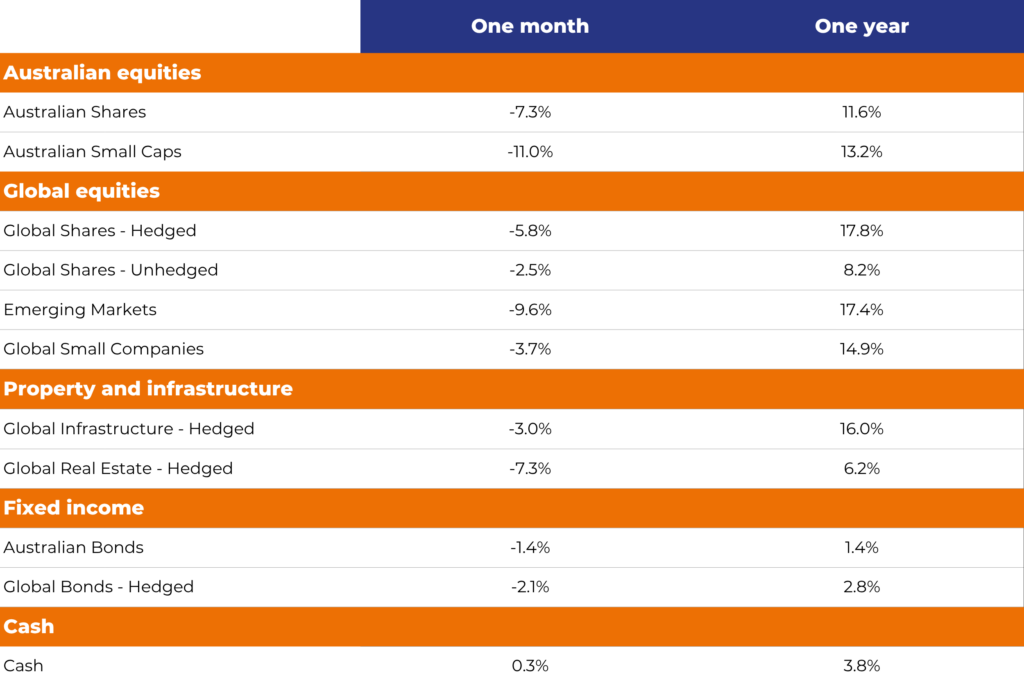

Australian shares fell 7.3% in March, the weakest monthly result since mid-2022. Technology stocks and financials bore the brunt of the selling, while energy and utilities were the only sectors to finish in positive territory supported by higher oil prices. March is typically the peak month of the ASX dividend season, with billions of dollars paid directly to shareholders as income, independent of any movement in the share price.

Globally, US shares fell just 1.2% in local currency terms, outperforming most other developed markets as a net energy exporter less exposed to the supply disruption. Europe fell 4.5% and emerging markets dropped 9.6%, both more affected by higher energy import costs. Australian small companies also had a difficult month, falling 11.0%.

The Australian dollar weakened against the US dollar during the month. For investors holding global shares without currency hedging, that actually softened the blow, as overseas assets are worth more in Australian dollar terms when the currency falls. Global shares returned -2.5% for unhedged investors compared to -5.8% for those with currency hedging in place.

Fixed interest

Bonds had a challenging month, with rising inflation and interest rate expectations pushing yields higher and prices lower. Australian bonds returned -1.4% for the month and global bonds -2.1%.

The income that bonds and cash are generating remains at its highest level in more than a decade. That income continues to flow regardless of short-term price movements and remains a meaningful component of returns for investors holding a mix of growth and defensive assets.

Winners and losers

It was a month with few winners. Energy was the standout, with Brent crude rising 77.6% and energy-related shares among the few parts of the market to post positive returns. Most other asset classes fell, with some losing less than others.

Emerging markets and Australian small companies were among the hardest hit, falling 9.6% and 11.0% respectively, as both are more sensitive to shifts in global risk appetite and higher energy import costs.

Listed property also had a difficult month. Australian REITs fell 11.2% and global REITs 7.3%, as rising bond yields reduced the relative attractiveness of property income. Gold fell 8.0% in March but has still returned 34.3% over the past year, supported by a weaker US dollar and ongoing political uncertainty.

Staying the course

Periods of market volatility, while uncomfortable, are part of the investment experience. Investors who remain disciplined through downturns and resist the urge to act on short-term movements have historically been well served. Selling into weakness locks in losses and often means missing the recovery. Staying invested in a diversified portfolio, built to navigate a range of market conditions, remains the most reliable path to meeting long-term objectives.

Asset class returns – March 2026

Since month end, investment markets have partially recovered from the March losses below, though conditions remain uncertain and we will continue to monitor developments closely.