MARKET AND ECONOMIC OVERVIEW

The December quarter was a volatile one from a markets perspective as investor sentiment finally capitulated on heightened concerns regarding the impact of trade wars on the global economy, US central bank tightening, and Chinese growth slowdown. As a result risk assets sold off including local and global equities, property & infrastructure, and riskier parts of the bond segment.

Economic data, particularly in export-led countries, began to turn down as the impact of trade wars began to take effect and fears Chinese growth may be slowing faster than previously expected. The Chinese still have plenty of ammunition in their toolkit to engineer a “soft landing”, but most remain cautious on the path in the short term.

Europe was hit particularly hard in light of ongoing Brexit issues which seemed to be heading to an impasse and potentially messy divorce from the EU. Most US economic data held up well, however, housing data was weaker on higher mortgage rates and economic growth fell, which set the scene for potentially lower economic growth in the next quarter in light of the one-time sugar hit of lower taxes and government stimulus rolling off from a year earlier.

Most of the action centred on the US central bank which flip-flopped around during the quarter in terms of their messaging to markets regarding where they are in their policy normalisation path. They did clear up most of that confusion towards the back end of the quarter where they raised rates in December, indicated that a slowdown in the path of rate rises was necessary and that any future rate moves would be data dependent, but the Governor stated that the reduction in their balance sheet remained on “autopilot”, subsequently a poor choice of words, which weren’t reflected in the minutes.

The political environment remained poor with President Trump further emboldened by the US midterm elections which saw the Democrats take the House and Republicans remain in control of the Senate. No doubt US politics gets messier from here, but history shows equity markets do well when politics is divided. We also saw a continuation of Brexit issues, riots in France, and the Italians threatening a rather large budget deficit outside of EU rules.

All in all, plenty of negative news flow. However, underlying economic data, whilst weakened, still remains in positive / expansionary territory and recession fears appear overhyped based on plenty of leading economic indicators, all whilst asset prices look a lot cheaper than they did three months ago.

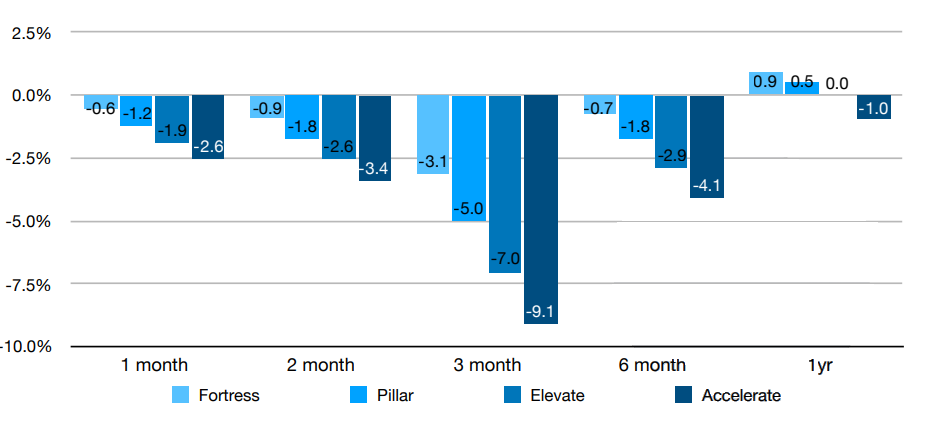

PORTFOLIO SUMMARY

In terms of the Portfolios, overall performance was a little disappointing relative to the high standards we set, though it’s very important not to focus on short term numbers when we’re investing for the long term. The main contributors were: investment selection in global equities, where all three investments outperformed their relevant benchmarks; asset allocation to both Australian and global listed property, which provide some downside relief from equities; and selection in the T. Rowe Price Dynamic Global Bond fund, which had a strong quarter given its defensive positioning. The main detractors included: the Australian small companies allocation, which was hurt by rising volatility; and investment selection within Bonds, with Macquarie Income Opportunities and PIMCO Diversified Fixed Interest producing reasonable but below benchmark results.

DIRECT AUSTRALIAN SHARE PORTFOLIO

In wake of the recent sell-off, results from the Bellmont Consolidated Equities portfolio have been muted, with a -0.3%*1 return since inception in late November 2017 unexciting, but still just over 1% better than the benchmark ASX200 Accumulation Index over the same period. For the 2019 FY so far our modest negative return of -0.27% stands head and shoulders above the -6.8% for the market as a whole, despite our portfolio falling 8.4% in the December quarter, almost in lockstep with the benchmark index.

On the portfolio front the biggest news of the quarter was the completion of the annual rebalance of the systematic portion of the portfolio. This half of the portfolio is managed according to a robust set of rules that have been developed based on decades of academic research, looking at both the quality and value of the 100 largest companies listed on the ASX. The rebalance provides us with an opportunity to trim or exit positions whose businesses have performed poorly, or no longer represent value relative to other candidates in the top 100. The proceeds of the sell down and dividends accumulated over the year are then reallocated to purchase stocks that are currently out of favour with the market, as well as potentially topping up existing positions which still represent good value.

Of the 16 holdings in the systematic side of the portfolio prior to the rebalance we ended up retaining 10 stocks – albeit with some minor changes to their weightings, while selling down 6 and replacing them with 5 new holdings that currently offer a better mix of quality and value. Notable transactions included the sale of two of our high flying holdings from the last 12 months – telecommunications company TPG Telecom (TPM) which had generated us a return in excess of 30%, and gold miner Northern Star Resources (NST) which had contributed almost 40% returns (note, we still hold a small position in TPG Telecom in the Classic Value side of the portfolio). Moving into the portfolio were global fund manager Pendal Group (PDL), packaging company Amcor Limited (AMC), soft drink bottler Coca-Cola Amatil (CCL), diversified property group Stockland (SGP) and global mining giant Rio Tinto (RIO).

On the positive side of the ledger, one of our newer holdings – leading Australian SaaS provider Technology One (TNE) defied the difficult market conditions, and delivered a solid 12% return for the quarter. While a 12% return over a 3 month period is always commendable, it was even more impressive in this case, occurring against a backdrop of rapidly falling markets, and weak sentiment towards technology stocks in particular. Pleasingly though, the rally wasn’t driven by erratic ‘animal spirits’, but the company’s 2018 FY earnings (their financial year ends in September, and they report to the ASX in November) which showed once again why we consider this company to be quite possibly the highest quality business on the ASX. Revenues, profits and margins were all up for the year, with earnings per share rising at a very respectable 14.6% rate. A growing proportion of the company’s revenues are now recurring, and the company’s customer retention is spectacular at over 99%. Capping it off is a rock-solid balance sheet with no debt and $104m in cash – ensuring that the business remains well enough capitalised to deal with any future contingency. While such positive share price movements are obviously wonderful from an ego perspective, we should all be hoping for the market to once again fall out of love with the company, so that the share price can fall back to a level where we could pick up more shares in this outstanding business.

Looking ahead to 2019, we have no idea whether share prices will recover strongly, stagnate at these levels or even continue to fall further. In the long run though, share prices will move in line with company earnings, and with the underlying businesses of our portfolio companies performing strongly and aggregate valuations of our holdings as attractive as they have been for quite some time, we are delighted to be close to fully invested, and are optimistic about long term future returns from these levels.

And that’s all for our December quarter update. As always we will be keeping a close eye on the portfolios, and will make any adjustments that might be necessary to maximise your long term returns. If you have any questions though, please feel free to contact your adviser who will be more than happy to help.

*1 Portfolio returns quoted are gross returns, excluding franking credits, before fees and costs

To find out more about our investment services, please visit our Investment Portfolio Management page here.

This advice may not be suitable to you because it contains general advice that has not been tailored to your personal circumstances. Please seek personal financial advice prior to acting on this information.

Synchron Privacy Policy

Investment Performance: Past performance is not a reliable guide to future returns as future returns may differ from and be more or less volatile than past returns.

Financial Framework Pty Ltd t/as Financial Framework ABN 34 465 945 965 are Authorised Representatives of Synchron AFS Licence No 243313