A common question for those in mid-career is whether it’s a good time to pay off an outstanding mortgage, or contribute more to their super or retirement fund.

While we have addressed this question before, the changing landscape in 2020 raises the question again, and perhaps changes the answer, depending on your situation.

Let’s look at the question in a new light, and why it’s worth revisiting.

Paying Off The Mortgage

People in their 40s and 50s often feel that it’s best to pay off the mortgage. In many instances, it makes good sense to eliminate debt. That’s especially true if it’s bad debt like credit card debt.

But in terms of a mortgage, it’s not always the case that paying it off first is the best solution. After all, everyone’s situations are different which makes it a little bit more complicated than a straight up yes or no answer.

For instance, if your mortgage isn’t your only debt or your superannuation isn’t your only investment, the answer to the question might not be so straightforward. If you have a personal loan, or other investments like an investment property, or other assets and liabilities, the more complicated things can be.

And perhaps you want to enter retirement without the burden and stress of a mortgage, also a good idea. But the answer again depends on your situation, such as how many years you have until you will retire. You may still be able to eliminate the mortgage debt before you retire, without doing it immediately.

Trends For Over 55’s

One thing to take notice of is the significant trend occurring in the number of people 55 years and over who are approaching retirement with a mortgage. Over the last 18 years, the number of people has doubled, with 47% of people over 55 now holding a mortgage. This does not indicate that it’s a bad thing to have a mortgage at this stage of life, however it’s something to be mindful of.

Dropping Interest Rates

Now let’s add in the fact that interest rates are dropping. This makes it even more interesting when you consider your options.

In March, 2020, the Reserve Bank of Australia (RBA), Australia’s central bank and banknote issuing authority, set its rate at .5%. As a result of COVID-19, the RBA cut rates again during March to .25% and in November rates were cut again to .10%.

These cuts by the RBA usually have a large impact on interest rates for mortgages.

Rather than paying your mortgage, you may want to consider refinancing, if the situation is right. You could take advantage of those lower interest rates to put more money toward the principal. In that way, you can pay it off faster, but not immediately. You could then contribute more to your super rather than pay off the mortgage in one step.

And one of the most important factors when considering whether to refinance a mortgage is what’s happening with the interest rates.

So as you can see, the answer is not a simple yes or no.

Dropping interest rates can have an impact on other investments, like term deposits. This is another area where you shouldn’t make a quick decision. Once again, there are no hard and fast rules that are best for everyone, but there are some things that you should avoid when rates drop on term deposits, like chase yield. But that’s a topic for another blog on things to consider when interest rates drop which you can read here.

It’s important to remember that everyone has a complex situation so it’s about how you wade through all that information.

Investing Your Super In The Markets

What’s happening in the investment markets may also have an influence over your decision at the time. During 2020, we have experienced unprecedented times in the investment markets. This is rather scary for some people and exciting for others.

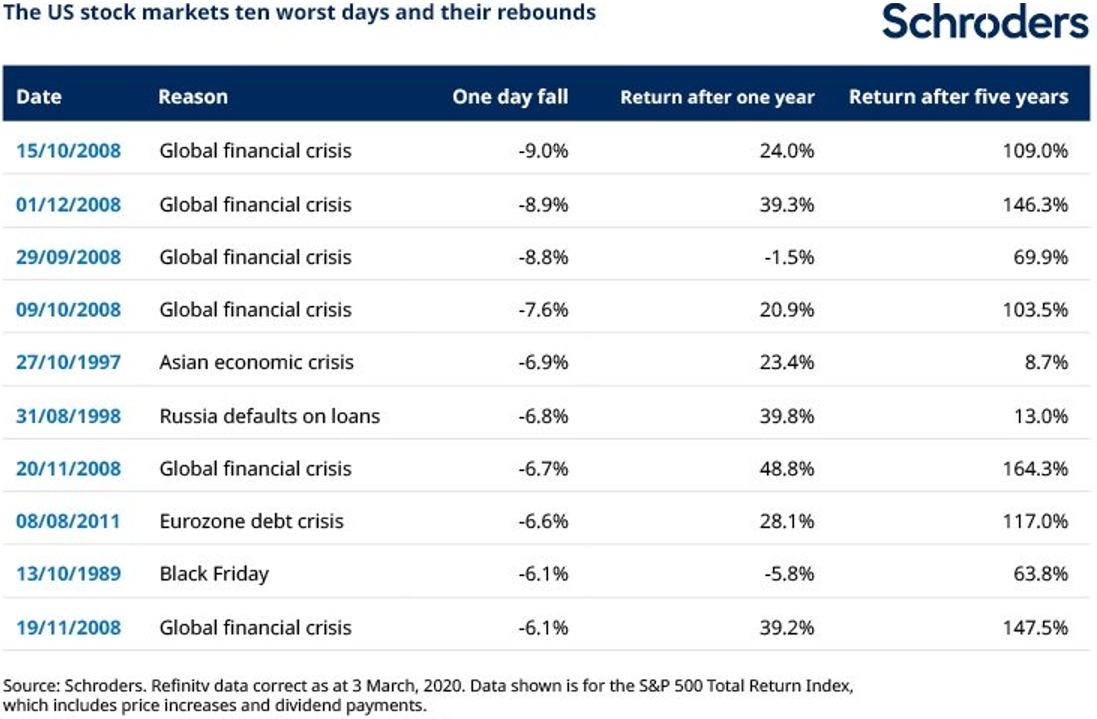

According to Schroders, big falls in the market can be followed by even bigger gains. And this has been a trend over the history of the share market.

(S&P 500 Total Returns)

For some people, this could be an ideal time to contribute more to their super in hope that they benefit on the upside more than they might have in regular times, when the market was trending upwards.

Although it does take a lot of confidence to invest during uncertain or declining markets, it can be of significant benefit over the long term if done correctly. You should always consult a professional on investing or superannuation when making significant investments or financial decisions.

Want to know more?

We have developed an eBook specifically to address this topic. To get your copy of the Ultimate Guide to Paying Off Your Mortgage and Topping Up Your Super, use the chat function to send us your details and we’ll send you a free copy.

Other Factors to Consider

There are three main factors to consider when determining whether to take any extra money and put it towards retirement savings or your mortgage:

- When do you want to retire?

- How much do you need in retirement?

- How much do you have now to put away?

And, as you prepare for retirement, there are other questions you should be asking, and not just whether to pay off your mortgage.

Here are some other discussions you might find worthwhile having with a certified financial adviser:

These are all great questions and something you should work through as you plan for the future.

If you’d like to discuss your entire financial picture, including your home mortgage, you can contact the advisers at Financial Framework and book a time to meet.